3 Emerging Fintech Trends in Southeast Asia

Discover 3 emerging fintech trends that are reshaping the financial landscape in Southeast Asia, driving innovation and access.

Discover 3 emerging fintech trends that are reshaping the financial landscape in Southeast Asia, driving innovation and access.

3 Emerging Fintech Trends in Southeast Asia

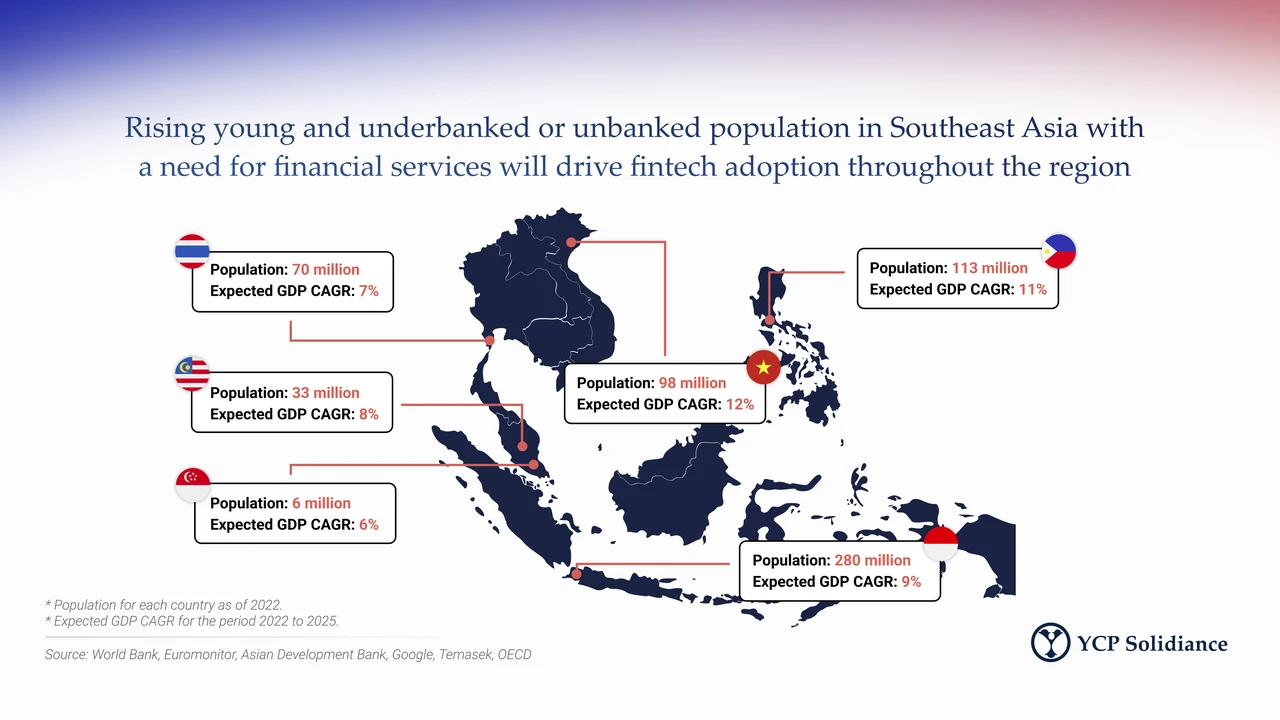

Southeast Asia is a vibrant and dynamic region, home to over 670 million people, many of whom are young, tech-savvy, and increasingly connected. This demographic, coupled with a significant unbanked and underbanked population, has created a fertile ground for financial technology, or fintech, to flourish. The region is not just adopting global fintech trends; it's innovating and adapting them to its unique economic and social contexts. From bustling urban centers to remote island communities, fintech is bridging gaps, empowering individuals, and transforming traditional financial services. Let's dive into three of the most impactful emerging fintech trends that are currently reshaping the financial landscape across Southeast Asia.

Digital Payments and E-Wallets Revolutionizing Transactions

The shift from cash to digital payments is perhaps the most visible and widespread fintech trend across Southeast Asia. E-wallets and mobile payment platforms have become ubiquitous, driven by smartphone penetration, e-commerce growth, and the convenience they offer. This trend is particularly significant in a region where a large portion of the population previously relied almost exclusively on cash, often lacking access to traditional banking services. Digital payments are not just about convenience; they're about financial inclusion, enabling millions to participate in the digital economy.

Key Players and Their Offerings in Digital Payments

The digital payments landscape in Southeast Asia is highly competitive, with numerous local and regional players vying for market share. Here are some of the leading platforms and what makes them stand out:

- GrabPay (Singapore, Malaysia, Indonesia, Philippines, Vietnam, Thailand): Part of the Grab super-app ecosystem, GrabPay is arguably one of the most dominant e-wallets in the region. It integrates seamlessly with Grab's ride-hailing, food delivery, and parcel delivery services, making it incredibly convenient for daily transactions. Users can top up their GrabPay wallets through various methods, including bank transfers, debit/credit cards, and even cash at convenience stores. GrabPay also offers loyalty programs and rewards, incentivizing its use. For example, in Singapore, users can earn GrabRewards points on every transaction, which can be redeemed for discounts on Grab services or partner merchants.

- GoPay (Indonesia): As the payment arm of Indonesia's tech giant Gojek, GoPay is a powerhouse in its home market. Similar to GrabPay, it's deeply integrated into the Gojek ecosystem, covering everything from ride-hailing and food delivery to bill payments and peer-to-peer transfers. GoPay has been instrumental in driving financial inclusion in Indonesia, reaching millions of users who were previously unbanked. It also offers features like GoPayLater, allowing users to pay for services later, and GoPay Coins for rewards.

- ShopeePay (Singapore, Malaysia, Indonesia, Philippines, Thailand, Vietnam): Emerging from the e-commerce giant Shopee, ShopeePay has rapidly expanded its reach. While initially focused on facilitating transactions within the Shopee platform, it has grown into a standalone e-wallet accepted by a wide network of offline merchants. ShopeePay often offers attractive cashback and discount vouchers, making it a popular choice for online shoppers and budget-conscious consumers. Its integration with Shopee's vast merchant network gives it a significant advantage.

- Touch 'n Go eWallet (Malaysia): A leading e-wallet in Malaysia, Touch 'n Go eWallet leverages the existing infrastructure of the Touch 'n Go card, widely used for toll payments and public transport. This strong foundation has allowed it to quickly gain traction. Beyond transport, it supports QR code payments at merchants, bill payments, and even peer-to-peer transfers. They've also introduced innovative features like GO+ for earning returns on idle wallet balance and GOinvest for micro-investments.

- GCash (Philippines): GCash, powered by Globe Telecom, is a dominant force in the Philippines. It offers a comprehensive suite of financial services, including remittances, bill payments, online shopping, and even micro-loans and insurance. GCash has been particularly effective in reaching the unbanked population, providing a crucial entry point into formal financial services. Its user-friendly interface and extensive network of cash-in/cash-out partners make it highly accessible.

Comparison and Use Cases

While these platforms share core functionalities, their strengths lie in their ecosystem integration and specific market focus. GrabPay and GoPay excel in the super-app model, offering a seamless experience across multiple daily services. ShopeePay is strong in e-commerce and offline retail, often providing the best deals for shoppers. Touch 'n Go eWallet has a strong foundation in transport and is expanding into broader financial services. GCash is a leader in financial inclusion, offering a wide range of services to a broad demographic.

Typical Use Cases:

- Daily Commute: Using GrabPay for Grab rides or Touch 'n Go eWallet for public transport.

- Food Delivery: Paying for your GoFood or GrabFood orders with GoPay or GrabPay.

- Online Shopping: Leveraging ShopeePay for cashback and discounts on Shopee.

- Bill Payments: Paying electricity, water, or internet bills directly through GCash or GoPay.

- Peer-to-Peer Transfers: Sending money to friends and family instantly using any of these e-wallets.

- Offline Retail: Scanning QR codes at local cafes, supermarkets, and hawker stalls.

The pricing for these services is generally low or free for basic transactions like peer-to-peer transfers and merchant payments. Revenue is often generated through transaction fees from merchants, premium services, and advertising within the apps. For example, some platforms might charge a small fee for cash-out transactions or for certain bill payments, but these are typically minimal to encourage widespread adoption.

Embedded Finance and Banking as a Service (BaaS) Expanding Financial Access

Embedded finance is a game-changer, integrating financial services directly into non-financial platforms and customer journeys. Think about buying a product online and being offered a 'buy now, pay later' (BNPL) option at checkout, or a small business getting a loan offer directly from their e-commerce platform. This trend is closely linked with Banking as a Service (BaaS), where licensed banks open up their infrastructure (APIs) to allow third-party fintechs and non-financial companies to build and offer financial products without needing their own banking license. In Southeast Asia, this is particularly powerful for reaching underserved segments and creating highly contextualized financial solutions.

How Embedded Finance and BaaS Work

Traditionally, if a company wanted to offer a financial product, they'd need to become a bank or partner with one in a very traditional, often slow, way. BaaS changes this by allowing fintechs to 'plug into' a bank's existing regulatory framework and infrastructure. This means a ride-hailing app can offer micro-loans to its drivers, or an e-commerce platform can provide insurance to its sellers, all powered by a bank in the background, but branded and delivered by the platform itself.

Impact and Examples in Southeast Asia

This trend is democratizing financial services and making them more accessible and relevant. Here are some examples:

- BNPL Services: Companies like Atome (Singapore, Malaysia, Indonesia, Vietnam, Philippines, Thailand) and PayLater by Grab/GoPayLater by Gojek are prime examples. They allow consumers to split purchases into interest-free installments, often at the point of sale, without needing a credit card. This is huge for consumers who might not qualify for traditional credit or prefer flexible payment options. Atome, for instance, partners with thousands of retailers, both online and offline, offering a seamless payment experience. The merchant pays a fee to Atome, typically a percentage of the transaction, while consumers enjoy interest-free installments as long as they pay on time.

- Embedded Lending: E-commerce platforms like Shopee and Lazada offer loans to their merchants based on their sales data and performance. This provides crucial working capital to small and medium-sized enterprises (SMEs) that often struggle to get financing from traditional banks due to lack of collateral or credit history. For example, Shopee Seller Centre might offer a 'Seller Loan' with competitive interest rates, directly integrated into the seller's dashboard. The interest rates and terms vary based on the seller's profile and loan amount, but they are generally designed to be more accessible than traditional bank loans.

- Embedded Insurance: Imagine buying a flight ticket and being offered travel insurance directly within the booking process, or purchasing a new phone and being offered device protection. Companies like Igloo (Singapore, Indonesia, Philippines, Thailand, Vietnam, Malaysia) are leaders in this space, partnering with e-commerce platforms, ride-hailing apps, and logistics companies to offer highly contextualized insurance products. For instance, a food delivery driver might be offered micro-insurance for their daily trips, or an e-commerce buyer might get parcel protection. The cost of these micro-insurance products is typically very low, often just a few dollars, making them affordable and attractive.

- Digital Banks leveraging BaaS: New digital banks in the region, such as TMRW by UOB (Thailand, Indonesia) or GXS Bank (Singapore, Malaysia – a joint venture between Grab and Singtel), often leverage BaaS principles to build their offerings. While they hold their own licenses, their agile technology stacks and API-first approach allow them to integrate with other services and offer highly personalized banking experiences. They often target specific segments, like young professionals or gig economy workers, with tailored products and lower fees compared to traditional banks.

The pricing models for embedded finance vary. BNPL providers typically charge merchants a fee (e.g., 2-8% of the transaction value) and consumers late fees if they miss payments. Embedded lenders charge interest on loans. Embedded insurance providers earn premiums. The key is that these services are offered at the point of need, making them highly convenient and often more accessible than traditional alternatives.

Blockchain and Decentralized Finance (DeFi) Innovations for Transparency and Efficiency

While still in its nascent stages compared to digital payments, the potential of blockchain and decentralized finance (DeFi) in Southeast Asia is immense. The region has shown a strong appetite for cryptocurrencies, and the underlying blockchain technology offers solutions for transparency, efficiency, and financial inclusion, particularly in cross-border transactions and asset management.

Understanding Blockchain and DeFi's Role

Blockchain is a distributed ledger technology that allows for secure, transparent, and immutable recording of transactions. DeFi takes this a step further, building financial applications on blockchain networks (like Ethereum or Binance Smart Chain) that operate without traditional intermediaries like banks. This means peer-to-peer lending, borrowing, trading, and even insurance can happen directly between users, often at lower costs and with greater speed.

Emerging Applications and Platforms

Southeast Asia is seeing a surge in blockchain and DeFi adoption, driven by a tech-savvy population and a desire for more efficient financial systems:

- Cryptocurrency Exchanges: Platforms like Binance (global presence, strong in SEA), Coinhako (Singapore), and Indodax (Indonesia) are popular gateways for individuals to buy, sell, and trade cryptocurrencies. These exchanges offer a range of digital assets, from Bitcoin and Ethereum to various altcoins. They typically charge trading fees (e.g., 0.1% to 0.5% per trade) and withdrawal fees. Many also offer staking services, allowing users to earn passive income on their crypto holdings.

- Cross-Border Remittances: Traditional remittances are often slow and expensive. Blockchain-based solutions are emerging to address this. For example, RippleNet, while not a direct consumer product, partners with financial institutions in the region (like Siam Commercial Bank in Thailand) to facilitate faster and cheaper cross-border payments using XRP. While not fully decentralized, it leverages blockchain principles for efficiency. More direct DeFi solutions for remittances are also being explored, allowing individuals to send stablecoins across borders with minimal fees and near-instant settlement.

- NFTs and Digital Assets: The non-fungible token (NFT) market has exploded globally, and Southeast Asia is no exception. Artists, creators, and collectors are using platforms like OpenSea (global) and local marketplaces to buy, sell, and trade unique digital assets. While not strictly a financial service, NFTs represent a new form of digital ownership and investment, often tied to cryptocurrencies. The fees involved typically include gas fees (transaction costs on the blockchain) and marketplace commissions (e.g., 2.5% on OpenSea).

- DeFi Lending and Borrowing Platforms: Platforms like Aave and Compound (global, accessible in SEA) allow users to lend out their cryptocurrencies to earn interest or borrow against their crypto collateral. These platforms operate on smart contracts, automating the lending process and removing intermediaries. The interest rates for lending and borrowing are dynamic, determined by supply and demand within the protocol. While these are global platforms, their accessibility to users in Southeast Asia, particularly those seeking alternatives to traditional banking, is significant.

- Central Bank Digital Currencies (CBDCs) Exploration: Several central banks in Southeast Asia, including those in Singapore, Thailand, and the Philippines, are actively exploring or piloting CBDCs. While not DeFi in the purest sense, CBDCs leverage blockchain-like technology to create a digital form of fiat currency, potentially improving payment efficiency, financial inclusion, and monetary policy implementation. For instance, Project Ubin in Singapore explored the use of distributed ledger technology for interbank payments.

Challenges and Opportunities

While the potential is vast, challenges remain, including regulatory uncertainty, scalability issues, and user education. However, the opportunity to create more transparent, efficient, and inclusive financial systems is a powerful driver for continued innovation in this space. The cost benefits of DeFi, particularly for cross-border transactions, are a major draw for a region with a large diaspora and significant remittance flows. The transparency offered by blockchain can also help combat corruption and build trust in financial systems.

The fintech landscape in Southeast Asia is evolving at an incredible pace. These three trends – digital payments, embedded finance, and blockchain/DeFi – are not just buzzwords; they are fundamental shifts that are democratizing financial services, fostering innovation, and ultimately empowering millions across the region. As technology continues to advance and regulatory frameworks adapt, we can expect even more transformative changes in how people manage, spend, and invest their money in this dynamic part of the world.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)