3 Essential Steps to Creating a Financial Plan

Learn 3 essential steps to create a comprehensive financial plan, guiding you towards your long term financial goals.

Learn 3 essential steps to create a comprehensive financial plan, guiding you towards your long term financial goals.

3 Essential Steps to Creating a Financial Plan

Hey there! Ever feel like your money is just… floating around? Like you're working hard, but not really seeing your financial future take shape? You're not alone. Many people feel overwhelmed by the idea of financial planning, thinking it's only for the super-rich or super-savvy. But guess what? It's for everyone, and it's not as complicated as you might think. Think of it like building a house: you wouldn't just start hammering nails, right? You'd need a blueprint. A financial plan is your personal blueprint for financial success, helping you understand where you are, where you want to go, and how to get there. It's about making intentional choices with your money so you can achieve your dreams, whether that's buying a home, retiring comfortably, sending your kids to college, or even just having a solid emergency fund. This isn't about deprivation; it's about empowerment. It's about taking control and making your money work for you. So, let's break it down into three essential, easy-to-understand steps. We'll cover everything from figuring out your current financial situation to setting smart goals and putting a solid action plan in place. We'll even dive into some practical tools and resources that can help you along the way. Ready to build your financial future? Let's get started!

Step 1 Assess Your Current Financial Situation Understanding Your Money Landscape

Before you can chart a course to your financial future, you need to know exactly where you stand right now. This isn't always the most fun part, but it's absolutely crucial. Think of it like a doctor's check-up for your finances. You need to know your financial 'health' before you can prescribe any treatments. This step involves gathering all your financial data, from income to expenses, assets to debts. It's about getting a clear, honest picture of your money landscape. Don't worry if it's not perfect; very few people's finances are. The goal here is clarity, not judgment.

Income and Expenses Tracking Your Cash Flow for Financial Clarity

First up, let's talk about your cash flow. This is the money coming in (income) and the money going out (expenses). Understanding this is fundamental. You need to know how much you earn and, more importantly, where every dollar is going. Many people are surprised when they actually track their spending. Those little daily coffees or subscriptions can add up fast!

How to Track Your Income and Expenses

- Manual Tracking: If you're old school, a simple spreadsheet or even a notebook can work. Just list all your income sources and categorize your expenses.

- Budgeting Apps: This is where technology shines. Apps can link directly to your bank accounts and credit cards, automatically categorizing transactions. They provide real-time insights and often have great visual dashboards.

- Bank and Credit Card Statements: Reviewing these monthly can give you a good overview, but it's less granular than dedicated tracking.

Recommended Budgeting Tools and Apps

Here are a few popular options that can make this process much easier:

- You Need A Budget (YNAB): This app is a fan favorite for a reason. YNAB uses a 'zero-based budgeting' philosophy, meaning every dollar is assigned a job. It's fantastic for getting really intentional with your spending. It has a bit of a learning curve, but once you get it, it's incredibly powerful. It costs around $14.99/month or $98.99/year after a free trial.

- Mint: A free and widely used app, Mint connects all your financial accounts in one place. It automatically categorizes transactions, tracks your spending, and helps you create budgets. It also monitors your credit score and alerts you to unusual spending. It's great for a comprehensive overview without the cost.

- Personal Capital (now Empower Personal Dashboard): While known for its investment tracking, Personal Capital also offers excellent free budgeting and cash flow analysis tools. It's particularly good if you have investments and want a holistic view of your net worth alongside your spending.

- PocketGuard: This app focuses on telling you 'how much you can spend' after accounting for bills, goals, and necessities. It's very user-friendly and great for those who want a quick, clear picture of their disposable income. It offers a free version with basic features and a paid 'PocketGuard Plus' for more advanced options (around $7.99/month or $79.99/year).

Comparison: YNAB is best for strict, intentional budgeting. Mint is great for a free, comprehensive overview. Personal Capital is ideal if you have investments and want a net worth tracker. PocketGuard is perfect for simplicity and knowing your 'safe to spend' amount.

Assets and Liabilities Calculating Your Net Worth for Financial Health

Next, let's look at your balance sheet. This involves listing everything you own (assets) and everything you owe (liabilities). Your net worth is simply your assets minus your liabilities. This number is a snapshot of your financial health at a given moment. It's a great indicator of your progress over time.

What are Assets?

Assets are things you own that have monetary value. They can be:

- Liquid Assets: Cash, checking accounts, savings accounts.

- Investments: Stocks, bonds, mutual funds, ETFs, retirement accounts (401k, IRA), brokerage accounts.

- Real Estate: Your home, rental properties.

- Personal Property: Cars, jewelry, collectibles (only include significant items that retain value).

What are Liabilities?

Liabilities are what you owe to others. These include:

- Debts: Credit card balances, student loans, car loans, personal loans.

- Mortgages: The outstanding balance on your home loan.

How to Calculate Your Net Worth

Simply add up the current market value of all your assets and subtract the total of all your liabilities. Do this regularly (e.g., quarterly or annually) to see your progress. Many of the budgeting apps mentioned above, especially Personal Capital, can automatically calculate and track your net worth for you.

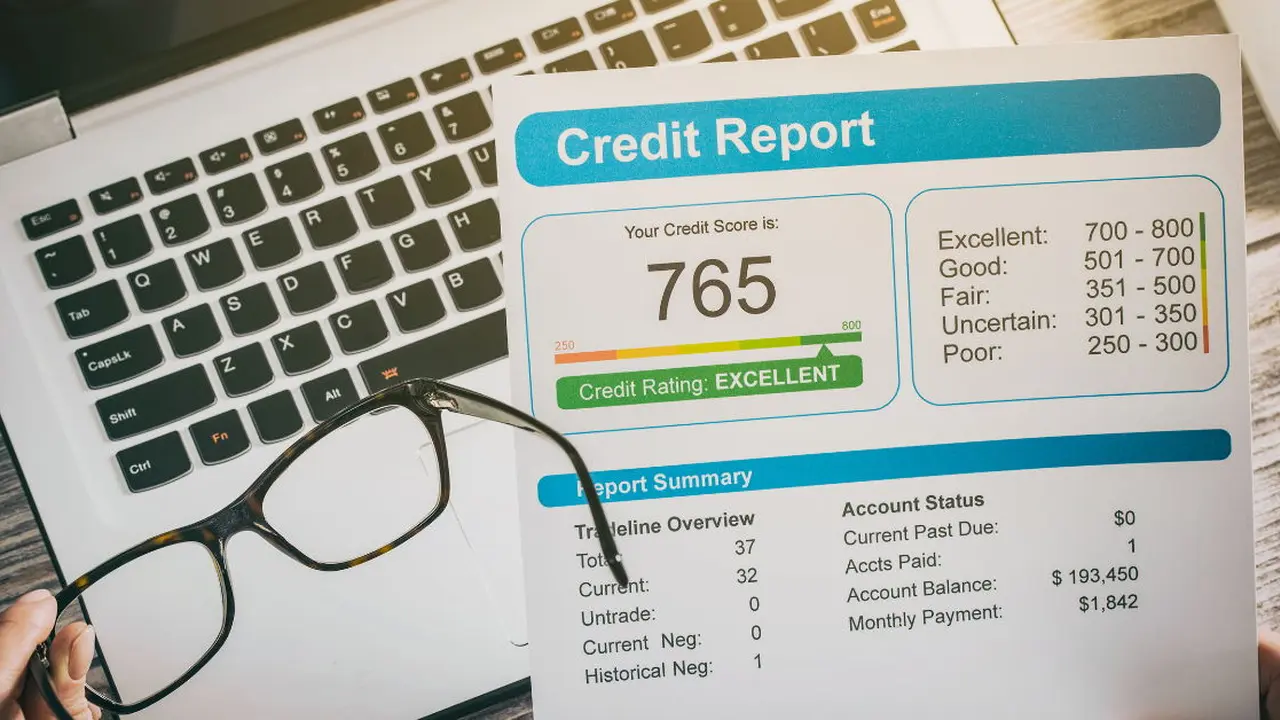

Credit Score and Report Understanding Your Financial Reputation

Your credit score is like your financial report card. It's a three-digit number that lenders use to assess your creditworthiness. A good credit score can save you thousands of dollars over your lifetime in lower interest rates on loans and credit cards. Your credit report is the detailed history that generates that score.

Why Your Credit Score Matters

- Loans and Mortgages: A higher score means better interest rates.

- Credit Cards: Access to premium cards with better rewards.

- Rentals: Landlords often check credit scores.

- Insurance Premiums: Some insurers use credit-based insurance scores.

- Employment: Some employers check credit as part of background checks.

How to Check Your Credit Score and Report

- Free Annual Credit Report: You are entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) once every 12 months at www.annualcreditreport.com. Review these carefully for errors.

- Credit Monitoring Services: Many banks and credit card companies offer free credit score monitoring. Apps like Credit Karma and Credit Sesame also provide free scores and reports (though often not FICO scores, but rather VantageScore, which is similar).

Pro Tip: Always check your credit reports for inaccuracies. Identity theft or reporting errors can negatively impact your score. Dispute any errors immediately.

Step 2 Define Your Financial Goals Setting SMART Objectives for Success

Once you know where you are, it's time to figure out where you want to go. This is the exciting part! Financial goals give your money a purpose. Without goals, you're just saving or spending aimlessly. But not all goals are created equal. To be effective, your financial goals should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

Short Term Goals Achieving Quick Wins and Building Momentum

Short-term goals are typically those you want to achieve within one to three years. These are great for building momentum and seeing tangible progress quickly.

Examples of Short Term Financial Goals

- Building an Emergency Fund: This is often the first and most crucial short-term goal. Aim for 3-6 months of living expenses in a high-yield savings account.

- Paying Off High-Interest Debt: Tackling credit card debt or other high-interest loans can free up significant cash flow.

- Saving for a Down Payment: For a car, a vacation, or a smaller purchase.

Medium Term Goals Planning for Significant Milestones

Medium-term goals usually fall within a three to ten-year timeframe. These are often bigger milestones that require more planning and consistent effort.

Examples of Medium Term Financial Goals

- Saving for a Home Down Payment: A larger sum than a car, requiring more dedicated saving.

- Funding a Child's Education: Starting a 529 plan or other education savings vehicle.

- Career Development: Saving for further education, certifications, or starting a business.

- Major Home Renovations: A new kitchen or an extension.

Long Term Goals Securing Your Future and Legacy

Long-term goals are those that are ten years or more away. These are often the biggest and most impactful goals, requiring consistent, disciplined effort over many years.

Examples of Long Term Financial Goals

- Retirement: This is usually the biggest long-term goal for most people.

- Financial Independence: Reaching a point where your investments generate enough income to cover your living expenses.

- Leaving a Legacy: Planning for inheritance or charitable giving.

Prioritizing Your Goals Aligning with Your Values and Timeline

You'll likely have multiple goals, and that's perfectly normal. The key is to prioritize them. Which ones are most important to you? Which ones have the biggest impact on your financial well-being? For example, building an emergency fund should almost always come before investing for retirement, because it provides a crucial safety net.

Tips for Prioritization

- Impact vs. Urgency Matrix: Which goals are both important and urgent?

- Financial Impact: Which goals will save you the most money (e.g., paying off high-interest debt)?

- Personal Values: Which goals align most with what truly matters to you?

Step 3 Create and Implement Your Action Plan Putting Your Financial Strategy into Motion

You've assessed your current situation, and you've set your goals. Now comes the most important part: taking action! A financial plan is useless if it just sits on paper. This step is about creating a roadmap and then consistently following it. It involves making concrete decisions about how you'll allocate your money, where you'll save and invest, and how you'll protect your assets.

Budgeting and Saving Allocating Resources for Your Goals

This is where your income and expense tracking from Step 1 really pays off. Now you can create a budget that reflects your goals. A budget isn't about restricting yourself; it's about giving every dollar a job, aligning your spending with your priorities.

Budgeting Strategies to Consider

- 50/30/20 Rule: A popular guideline where 50% of your income goes to needs, 30% to wants, and 20% to savings and debt repayment. This is a great starting point for many.

- Zero-Based Budgeting: As mentioned with YNAB, every dollar is assigned a category. This ensures no money is left unaccounted for.

- Pay Yourself First: Automate your savings and investments before you even see the money. This ensures you prioritize your financial goals.

Automating Your Savings and Investments

This is perhaps the single most effective strategy for achieving financial goals. Set up automatic transfers from your checking account to your savings, investment, and retirement accounts. Out of sight, out of mind – in a good way!

Investing for Growth Building Wealth Over Time

Once you have an emergency fund in place and are managing high-interest debt, it's time to think about investing. Investing is how your money works for you, growing over time through compound interest. Don't be intimidated; you don't need to be a stock market guru to start.

Types of Investment Accounts

- Retirement Accounts: 401(k)s, IRAs (Traditional and Roth). These offer significant tax advantages.

- Brokerage Accounts: For general investing, allowing you to buy stocks, ETFs, mutual funds, etc.

- 529 Plans: For education savings.

Investment Platforms and Robo-Advisors

For beginners, robo-advisors are an excellent choice. They manage your investments based on your risk tolerance and goals, often with low fees.

- Betterment: A pioneer in robo-advising, Betterment offers diversified portfolios of ETFs, automatic rebalancing, and tax-loss harvesting. It's great for hands-off investing. Fees are 0.25% of assets under management (AUM) for balances under $100k, and 0.40% for balances over $100k for their premium plan. Minimum to start is $0.

- Wealthfront: Similar to Betterment, Wealthfront also offers automated investing with diversified ETF portfolios, tax-loss harvesting, and even a high-yield cash account. It's known for its sophisticated financial planning tools. Fees are 0.25% AUM. Minimum to start is $500.

- Fidelity Go: Fidelity's robo-advisor offers a blend of human advice and automated investing. It's a good option if you prefer a well-established financial institution. Accounts under $25,000 are managed for free; over that, it's 0.35% AUM. Minimum to start is $0.

- Vanguard Digital Advisor: Known for its low-cost index funds, Vanguard's robo-advisor offers a cost-effective way to invest. Fees are around 0.15% AUM. Minimum to start is $3,000.

Comparison: Betterment and Wealthfront are top-tier pure robo-advisors with excellent features. Fidelity Go offers a hybrid approach with human advice. Vanguard Digital Advisor is the most cost-effective for those who prefer Vanguard's investment philosophy.

Protecting Your Assets and Future Insurance and Estate Planning

Financial planning isn't just about growing your money; it's also about protecting it and ensuring your loved ones are taken care of. This involves insurance and estate planning.

Essential Insurance Coverage

- Health Insurance: Non-negotiable in most places.

- Auto Insurance: Legally required in most states.

- Homeowners or Renters Insurance: Protects your dwelling and belongings.

- Life Insurance: Especially important if you have dependents.

- Disability Insurance: Protects your income if you can't work due to illness or injury.

Estate Planning Basics

This might sound like something only for the wealthy, but everyone needs a basic estate plan. It ensures your wishes are carried out if you become incapacitated or pass away.

- Will: Dictates how your assets are distributed.

- Power of Attorney: Designates someone to make financial decisions on your behalf if you can't.

- Healthcare Directive (Living Will): Specifies your wishes for medical treatment.

Online Estate Planning Tools

You don't necessarily need an expensive lawyer for basic estate planning. Several online services can help.

- LegalZoom: Offers various legal documents, including wills, powers of attorney, and living wills, at a more affordable price than a traditional lawyer. A basic will package can start around $89.

- Rocket Lawyer: Similar to LegalZoom, providing customizable legal documents and access to legal advice. A basic will can be created for free with a trial, then around $39.99/month for membership.

- Trust & Will: Specializes specifically in estate planning documents, offering user-friendly interfaces for creating wills and trusts. A will-based plan starts at $159.

Comparison: LegalZoom and Rocket Lawyer offer a broader range of legal services. Trust & Will is highly specialized in estate planning, making it very focused and user-friendly for this specific need.

Regular Review and Adjustment Keeping Your Plan Dynamic

Your financial plan isn't a static document. Life happens! Your income might change, you might have a new family member, or your goals might evolve. It's crucial to review and adjust your plan regularly.

When to Review Your Financial Plan

- Annually: A good general cadence to check in on your progress.

- Major Life Events: Marriage, divorce, birth of a child, job change, buying a home, inheritance.

- Significant Market Changes: While you shouldn't panic, understanding how market shifts affect your investments is important.

Why Adjustments are Necessary

Adjustments ensure your plan remains relevant and effective. Maybe you're ahead of schedule on one goal and need to reallocate funds, or perhaps you're behind and need to make some spending cuts. Flexibility is key.

So there you have it! Three essential steps to creating a financial plan that actually works for you. It might seem like a lot at first, but remember, you don't have to do it all at once. Take it one step at a time. Start by understanding your current situation, then set those SMART goals, and finally, put your action plan into motion. The most important thing is to start. Even small steps today can lead to massive financial progress down the road. Your future self will thank you for taking control of your money now. Happy planning!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)