3 Essential Steps to Reviewing Your Credit Report

Follow these 3 essential steps to regularly review your credit report, ensuring accuracy and protecting your financial health.

Follow these 3 essential steps to regularly review your credit report, ensuring accuracy and protecting your financial health. It's not just about checking a score; it's about understanding the narrative of your financial life and safeguarding your future.

3 Essential Steps to Reviewing Your Credit Report

Hey there! Let's talk about something super important for your financial well-being: your credit report. Think of it as your financial report card, but way more detailed and with real-world consequences. Regularly reviewing your credit report isn't just a good idea; it's a crucial habit for anyone looking to maintain financial health, catch errors, and protect themselves from identity theft. We're going to break it down into three essential, easy-to-follow steps. No jargon, just practical advice.

Understanding Your Credit Report What It Is and Why It Matters

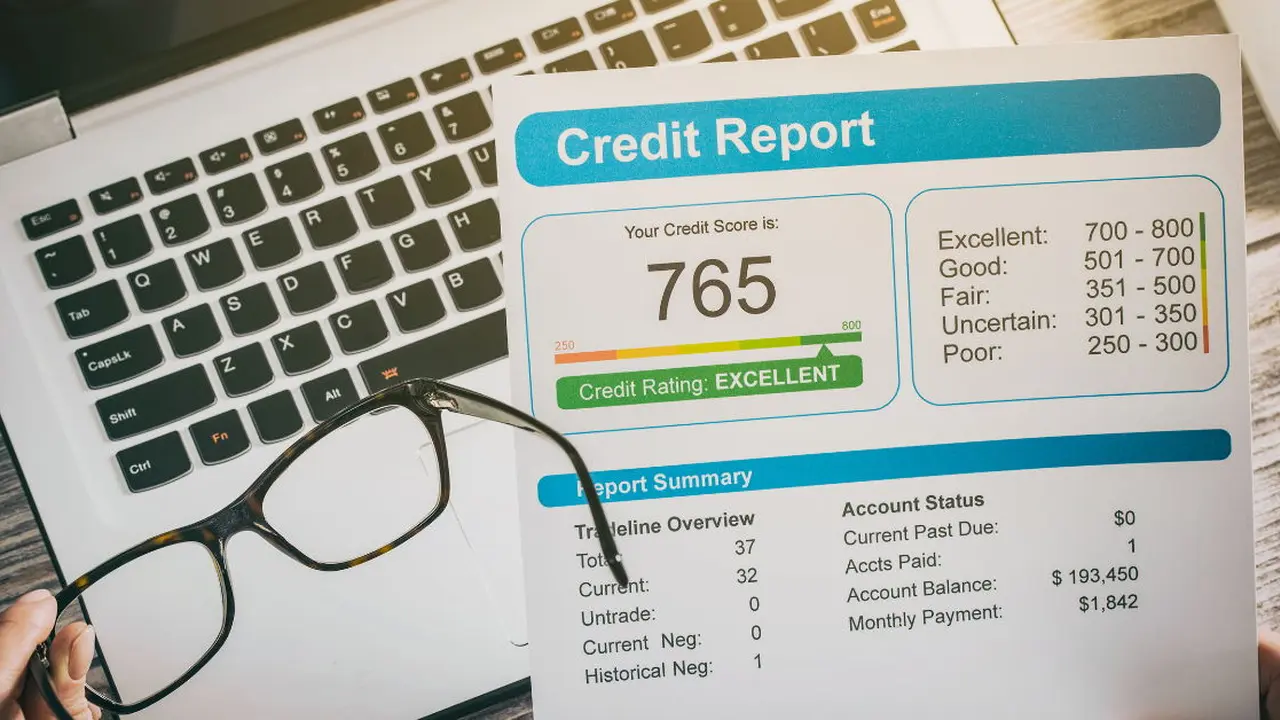

Before we dive into the 'how,' let's quickly cover the 'what' and 'why.' Your credit report is a detailed summary of your credit history. It includes information about your loans, credit cards, payment history, and even public records like bankruptcies. This report is used by lenders, landlords, employers, and even insurance companies to assess your financial reliability. A good credit report can open doors to better interest rates, easier loan approvals, and even lower insurance premiums. A bad one? Well, it can make life a lot harder.

There are three major credit bureaus in the U.S.: Equifax, Experian, and TransUnion. Each bureau collects and maintains its own version of your credit report. While they often contain similar information, there can be discrepancies, which is why checking all three is so important. In Southeast Asia, the landscape varies by country. For example, in Singapore, you have the Credit Bureau Singapore (CBS); in Malaysia, there's CTOS and Experian (formerly RAM Credit Information); and in the Philippines, the Credit Information Corporation (CIC). While the names and specifics differ, the core function remains the same: to provide a comprehensive view of your creditworthiness.

Step 1 Accessing Your Credit Reports Annually and Securely

The first and most fundamental step is getting your hands on your credit reports. And guess what? You're entitled to them for free! In the U.S., federal law grants you the right to one free credit report from each of the three major credit bureaus every 12 months. The official, government-mandated website for this is AnnualCreditReport.com. Don't be fooled by other sites that might try to charge you or sign you up for unwanted services. This is the only truly free and authorized source.

How to Get Your Free Credit Reports in the US

Go to AnnualCreditReport.com. You can request all three reports at once, or you can space them out throughout the year (e.g., Experian in January, Equifax in May, TransUnion in September) to monitor your credit more frequently. When you request your reports, you'll need to provide some personal information to verify your identity, such as your name, address, date of birth, and Social Security number. This is standard procedure to ensure you're the only one accessing your sensitive data.

Accessing Credit Reports in Southeast Asia

For our friends in Southeast Asia, the process is similar but varies by country:

- Singapore: You can obtain your credit report from the Credit Bureau Singapore (CBS) website (creditbureau.com.sg) or at their office. There's usually a small fee involved, but it's a crucial investment.

- Malaysia: CTOS (ctoscredit.com.my) and Experian (formerly RAM Credit Information) are the main players. You can typically get a basic report for free or a more detailed one for a fee.

- Philippines: The Credit Information Corporation (CIC) is the central repository. You can request your credit report through accredited credit bureaus or directly from the CIC.

- Thailand: The National Credit Bureau (NCB) provides credit reports. You can request them online or at designated service points.

- Indonesia: The Financial Services Authority (OJK) oversees credit information. You can access your credit report (Sistem Layanan Informasi Keuangan - SLIK) through their portal or at OJK offices.

Always check the official websites of the respective credit bureaus in your country for the most up-to-date information on how to access your report and any associated fees. Remember, accessing your own credit report is a 'soft inquiry' and does not negatively impact your credit score.

Step 2 Thoroughly Reviewing Your Credit Report for Accuracy and Errors

Once you have your credit reports in hand (or on screen), it's time to put on your detective hat. This isn't a quick skim; it's a detailed examination. Errors on your credit report are surprisingly common, and even a small mistake can significantly impact your credit score and financial opportunities. You're looking for anything that doesn't look right, anything that isn't yours, or anything that seems outdated.

Key Sections to Scrutinize in Your Credit Report

Your credit report is typically divided into several sections. Here's what to pay close attention to:

- Personal Information: Check your name, address, date of birth, and Social Security number (or national ID in Southeast Asia). Make sure everything is accurate and up-to-date. Incorrect information here could lead to mixed files with someone else's credit history.

- Credit Accounts (Tradelines): This is the meat of your report. It lists all your credit cards, loans (mortgages, auto loans, student loans, personal loans), and lines of credit. For each account, verify the following:

- Account Number: Ensure it's yours.

- Creditor Name: Is it a company you've done business with?

- Account Status: Is it open, closed, paid off, or delinquent?

- Payment History: This is critical. Look for any late payments that you know you made on time. Even a 30-day late payment can ding your score.

- Credit Limit/Loan Amount: Is it correct?

- Balance: Does it reflect what you owe?

- Date Opened/Closed: Are these dates accurate?

- Public Records: This section includes bankruptcies, foreclosures, tax liens, and civil judgments. Verify that any entries here are accurate and belong to you.

- Inquiries: This lists everyone who has requested your credit report. There are two types:

- Hard Inquiries: These occur when you apply for new credit (loan, credit card). Too many hard inquiries in a short period can slightly lower your score. Make sure you recognize all hard inquiries.

- Soft Inquiries: These happen when you check your own credit, or when a lender pre-approves you for an offer. Soft inquiries don't affect your score.

Common Errors to Look For

- Incorrect Personal Information: Misspellings, wrong addresses, or an incorrect date of birth.

- Accounts You Don't Recognize: This is a major red flag for identity theft.

- Incorrect Account Status: An account you paid off still showing as open or delinquent.

- Late Payments You Didn't Make: Disputed payments or payments that were actually on time.

- Incorrect Credit Limits or Loan Amounts: This can affect your credit utilization ratio.

- Duplicate Accounts: The same account listed multiple times.

- Outdated Information: Negative information (like a bankruptcy) that should have fallen off your report after a certain period (typically 7-10 years).

Step 3 Disputing Errors and Protecting Your Financial Health

Finding an error can be frustrating, but don't panic! The good news is that you have the right to dispute inaccurate information, and the credit bureaus are legally obligated to investigate. This step is crucial for correcting your record and safeguarding your financial health.

How to Dispute Errors in the US

If you find an error on your credit report, you should dispute it with both the credit bureau that issued the report and the creditor that reported the information. Here's the general process:

- Contact the Credit Bureau: Each credit bureau has a formal dispute process. You can typically do this online, by mail, or by phone. Online is often the quickest. Provide them with all the details of the error and any supporting documentation you have (e.g., bank statements, canceled checks, letters from creditors). Be specific about what information is inaccurate and why.

- Contact the Creditor: It's also a good idea to contact the creditor (the bank, credit card company, etc.) directly. They might be able to correct the error on their end, which can speed up the process.

- Keep Records: Document everything! Keep copies of your credit reports, dispute letters, any correspondence with the credit bureaus or creditors, and notes from phone calls (including dates, times, and names of people you spoke with).

- Follow Up: Credit bureaus typically have 30 days (sometimes 45 days if you provide additional information during the investigation period) to investigate your dispute. If they find an error, they must correct it and notify you. If they don't, or if they determine the information is accurate, they must provide you with a written explanation.

Disputing Errors in Southeast Asia

The dispute process in Southeast Asian countries follows a similar logic:

- Singapore (CBS): You can submit a dispute request directly through the CBS website or by mail. They will investigate with the relevant financial institution.

- Malaysia (CTOS/Experian): Both CTOS and Experian have online dispute resolution portals. You'll need to provide details and supporting documents.

- Philippines (CIC): Disputes are typically handled through the accredited credit bureaus that provided you with the report, or directly with the CIC.

- Thailand (NCB): The NCB has a dispute process, often requiring you to submit a form and supporting evidence.

- Indonesia (OJK): You can submit complaints or disputes regarding credit information through the OJK's consumer protection services.

Always refer to the specific credit bureau's website in your country for their exact dispute procedures and required documentation.

Beyond the Basics Credit Monitoring Services and Identity Theft Protection

While annual checks are essential, some people opt for continuous credit monitoring services. These services typically alert you to significant changes on your credit report, such as new accounts opened in your name, large inquiries, or changes in your credit score. This can be a proactive way to catch identity theft early.

Popular Credit Monitoring Services in the US

Many companies offer credit monitoring, often bundled with identity theft protection. Here are a few well-known ones, along with their general features and pricing (note: pricing can change, so always check their official sites for the latest info):

- IdentityForce (now part of TransUnion):

- Features: Comprehensive identity theft protection, 3-bureau credit monitoring, credit reports and scores, dark web monitoring, lost wallet assistance, identity theft insurance.

- Use Case: Best for individuals or families seeking robust identity theft protection alongside credit monitoring.

- Comparison: Often considered one of the most comprehensive options, with strong identity restoration services.

- Estimated Price: Starts around $17.99/month for individual plans.

- Experian IdentityWorks:

- Features: Experian credit report and FICO score, daily credit monitoring, dark web surveillance, identity theft insurance, fraud resolution support. Higher tiers include 3-bureau monitoring.

- Use Case: Good for those who want to focus on Experian's data primarily, or who are already Experian customers.

- Comparison: Direct from one of the major bureaus, offering deep insights into Experian data.

- Estimated Price: Basic plans start free (for Experian credit score), premium plans with more features around $9.99 - $19.99/month.

- Credit Karma:

- Features: Free credit scores (VantageScore 3.0 from TransUnion and Equifax), credit monitoring, identity monitoring, financial tools, and personalized recommendations.

- Use Case: Excellent free option for basic credit monitoring and understanding your scores.

- Comparison: While it doesn't offer FICO scores or 3-bureau reports, it's invaluable for regular, free monitoring and insights.

- Estimated Price: Free.

- MyFICO:

- Features: Access to all 28 FICO score versions, 3-bureau credit reports and monitoring, identity theft protection, FICO score simulator.

- Use Case: Ideal for those who need to know their exact FICO scores (which most lenders use) and want comprehensive monitoring.

- Comparison: The go-to for FICO scores, offering unparalleled detail and accuracy for lending decisions.

- Estimated Price: Plans start around $19.95/month.

Credit Monitoring in Southeast Asia

Credit monitoring services are also emerging and growing in popularity across Southeast Asia, though the offerings might be more localized:

- Singapore (CBS): CBS offers a subscription service called 'My Credit Monitor' which provides alerts on changes to your credit report.

- Malaysia (CTOS/Experian): Both CTOS and Experian offer personal credit monitoring services that alert you to new credit applications, changes in credit limits, or adverse records.

- Philippines (CIC): While direct monitoring services from CIC are still developing, some accredited credit bureaus might offer similar alert services.

- Thailand (NCB): The NCB provides a service called 'Credit Bureau Check' which allows for regular monitoring.

Always research and compare services available in your specific country, as features and pricing can vary significantly. Look for services that offer real-time alerts, comprehensive report access, and robust identity theft resolution support if that's a concern.

Why Regular Review is Your Best Defense Against Identity Theft and Financial Fraud

In today's digital age, identity theft and financial fraud are unfortunately common. Your credit report is often the first place where signs of fraudulent activity appear. An unfamiliar account, an inquiry you didn't authorize, or a sudden drop in your credit score could all be indicators that someone else is using your identity. By regularly reviewing your reports, you become your own first line of defense. Catching these issues early can save you countless hours of stress and potential financial losses.

Think of it as a regular health check-up for your finances. You wouldn't skip your annual physical, right? Your credit report deserves the same attention. It's not just about fixing mistakes; it's about empowering yourself with knowledge and control over your financial narrative. So, make it a habit. Mark your calendar. Set reminders. Your financial future will thank you for it.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)